Analyzing the ‘Recession Trade’ that surfaced in May

June 3rd, 2022 | Posted in Investing

Inside the ‘Recession Trade’ that Surfaced in May

The month of May has been characterized by selling pressure across just about every asset class, and a closer look shows investors shifting into a defensive crouch.

By Friday, May 20, the broad market as measured by the S&P 500 was off by -6.4%, the tech-heavy Nasdaq had plunged -8.7%, and the Russell 2000 index—a benchmark for small-cap stocks—had fallen by -6.0%. Even the S&P Consumer Staples sector, which had largely been shielded from exaggerated selling pressure, posted an -8.6% decline in the week ending May 20.1

But not all areas of the market took a beating. Traditionally defensive areas of the stock market, like the Utilities and Healthcare sectors, performed far better. Over the same time period, Utilities actually rose +0.3% and Healthcare fell by a modest -0.5%. This week’s column is not about the benefits of diversification, but readers can clearly see the example of how a broadly diversified portfolio can help smooth out returns.

Are Robo Advisors the Next Generation For Investment Management?

Robo advisors have made a splash by helping to streamline the investing process and possibly saving investors money. But can they replace the active management and personal attention of a traditional wealth manager? Our free Revolutionize Your Retirement guide takes a look at these important issues and more, providing our insights that may be able to help you make better investing choices. You’ll get our thoughts on:

- The Impact of Fees on Investments

- Technological Advantages including Rebalancing and Tax Loss Harvesting

- Combining Robo Technology with Active Management

Download your copy of Revolutionize Your Retirement.2

Prior to the past couple of weeks, stocks and bonds had also been falling in tandem. As we wrote in our last edition of Investor’s Advantage, through the first quarter of 2022, the S&P 500 index was down roughly -13% while the Bloomberg U.S. Aggregate bond index—which is comprised mostly of U.S. Treasuries, mortgage-backed securities, and investment grade corporate bonds—had declined by -10%. These two asset classes do not usually fall in such dramatic lockstep.

But the month of May has presented a different story, as stocks and bonds have decoupled to date. The yield on the 10-year U.S. Treasury seemed to peak on May 5 at 3.12%, but over the past two weeks, it has declined sharply to under 2.90% as bond prices rose. This apparent ‘flight to safety’ seemed to suggest that investors were now more worried about growth than they were about inflation. This shift, along with the outperformance of the defensive Utilities and Healthcare sectors, is what some are deeming the ‘recession trade’ that surfaced in May.

The question for investors is whether this ‘recession trade’ stems from an actual acute risk of recession, or (as is the case in almost all stock market corrections) a sell-off that is more related to changes in investor sentiment than to changes in economic fundamentals. We continue to think it’s the former.

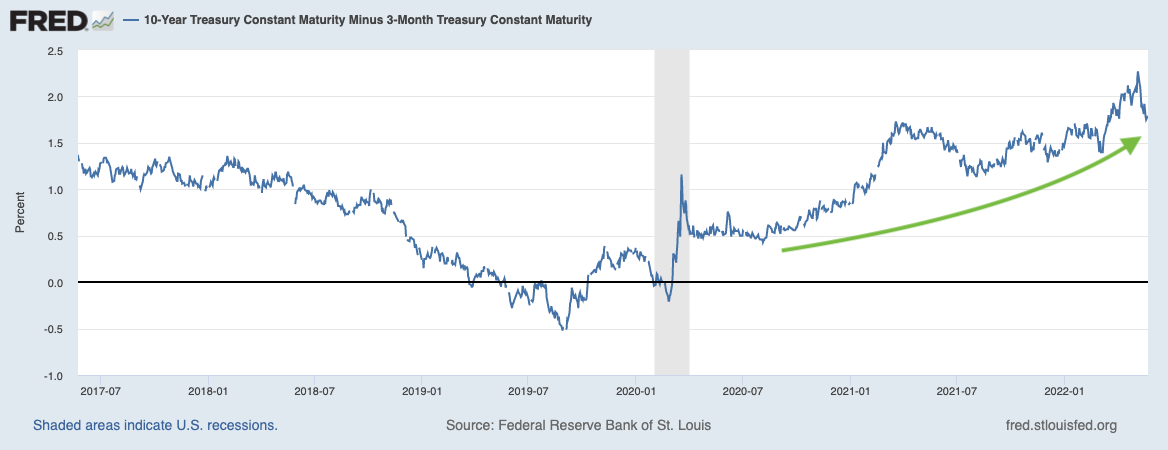

The recession chatter accelerated when elevated inflation readings collided with the war in Ukraine, which sent oil prices sharply higher. But the real recession talk began in earnest when the 10-year/2-year yield curve—which measures the difference in yield between the 10-year U.S. Treasury bond and the 2-year U.S. Treasury bond—inverted. The chart below shows when the inversion took place in early April:

The issue with this analysis, in our view, is that a better measure of the yield curve compares the 10-year U.S. Treasury bond yield with the 3-month U.S. Treasury bond yield, as this comparison more accurately reflects what’s happening with bank net interest margins. As you can see from the chart below, not only has the yield curve not inverted, it has been steepening in 2022—generally a harbinger of good growth conditions ahead.

As Blackrock points out, there is also a “labor market-sized hole in the theory of a U.S. recession….Not only does a tight labor market continue to support robust consumption, but ironically, this labor shortage and short-term inflationary impulse creates the need for investment in automation and other productivity-enhancing technology that will ultimately be disinflationary in the long run.”5

In April, the U.S. economy added another 428,000 jobs, which marks a full year of consecutive job gains above 400,000. The unemployment rate now sits at 3.6%, which is basically right where it left off in early 2020 before the pandemic struck (and when the economy was in good shape). A good jobs market bodes well for U.S. consumers, who remain in a strong financial position with lower debt loads, high job availability, and rising wages. These are not conditions that generally precede recessions.

Bottom Line for Investors

So, what is a ‘recession trade’ if there is no recession? In our view, the frenzied selling action more closely resembles what we see in pronounced market corrections, which are sharp, often scary pullbacks as investors react in real time to worrisome headlines. Even if U.S. stocks cross into technical bear market territory, with a decline of -20% or more, we do not see the market grinding lower over several months in response to a forthcoming economic recession—which is what bear markets do. The U.S. economy is poised to grow in 2022, carried forward by a strong labor market and a healthy consumer. Stocks should eventually do the same.

Today, innovative technology is changing the investment landscape quickly, including making investing for retirement potentially less complicated and more effective. Zacks Advantage is at the forefront of these developments with innovative investment solutions—including retirement investment solutions—using new financial technologies. We now offer an actively managed robo advisor that:

- Invests exclusively with ETFs

- Uses technology to recommend the appropriate mix of equities and bond ETFs to help achieve your investing goal and specific risk tolerance.

- Lowers fees and expenses

Our free Revolutionize Your Retirement guide6 provides investing insight that can help you determine whether technology-enhanced investing is right for you.

1Wall Street Journal. May 20, 2022.

2Zacks Investment Management may amend or rescind the Revolutionize Your Retirement guide offer for any reason and at Zacks Investment Management’s discretion.

3Fred Economic Data. May 24, 2022.

4Fred Economic Data. May 26, 2022.

6Zacks Investment Management may amend or rescind the Revolutionize Your Retirement guide offer for any reason and at Zacks Investment Management’s discretion.

Past performance is no guarantee of future results. Inherent in any investment is the potential for loss

Zacks Advantage is a service offered by Zacks Investment Management, a wholly-owned subsidiary of Zacks Investment Research. Zacks Investment Management is an independent Registered Investment Advisory firm and acts as an investment manager for individuals and institutions. All material in presented on this page is for informational purposes only and no recommendation or advice is being given as to whether any investment or strategy is suitable for a particular investor. Nothing herein constitutes investment, legal, accounting or tax advice. The information contained herein has been obtained from sources believed to be reliable but we do not guarantee accuracy or completeness. Zacks Investment Management, Inc. is not engaged in rendering legal, tax, accounting or other professional services. Publication and distribution of this article is not intended to create, and the information contained herein does not constitute, an attorney- client relationship. Do not act or rely upon the information and advice given in this publication without seeking the services of competent and professional legal, tax, or accounting counsel.